It was forecasted that the US Federal Reserve (Fed) would cut interest rates in March, and then other central banks, including the European Central Bank (ECB), would follow suit. But their chairman, Jerome Powell, poured cold water on it: “I don’t see it likely that rates will be cut in March.

For now, inflation is reluctant to drop below 3% in the United States, making interest rate cuts difficult.

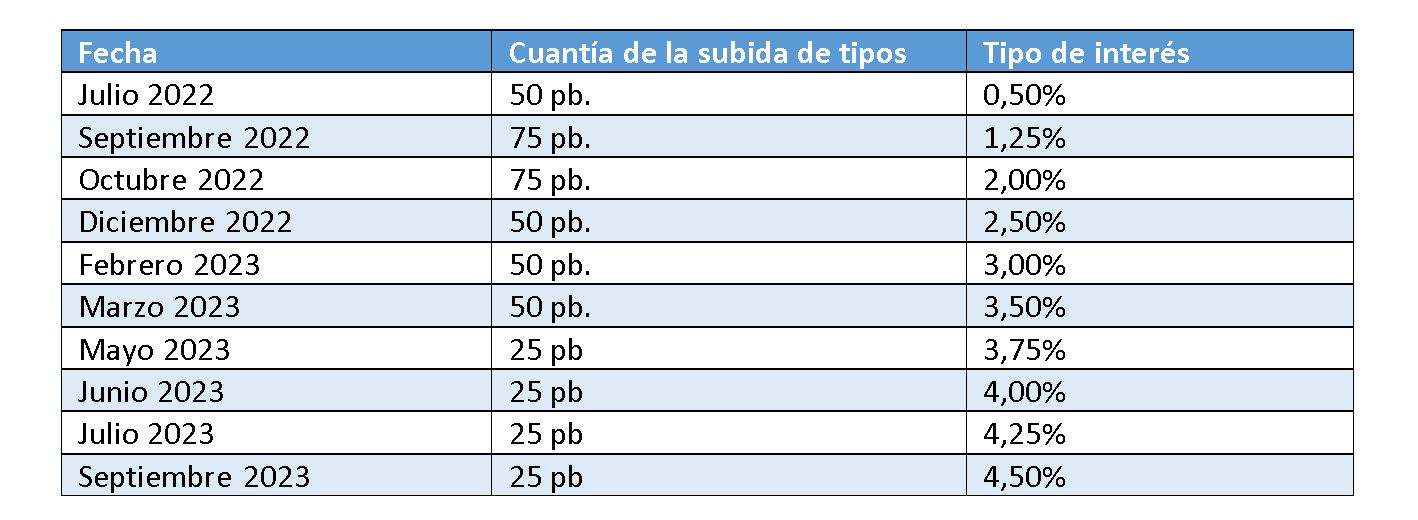

Therefore, it will still be some time before we see a new line with an interest rate cut in the following table, which shows the last 10 interest rate hikes implemented by the ECB to combat inflation, which surged after Covid-19 and the outbreak of the war in Ukraine:

There has been too much optimism about interest rate cuts

Interbank market heavily influenced by expectations; forecasts suggesting that rate cuts are being pushed further into the future and won’t be as pronounced as expected lead the market to immediately recover lost positions by the Euribor in previous months.

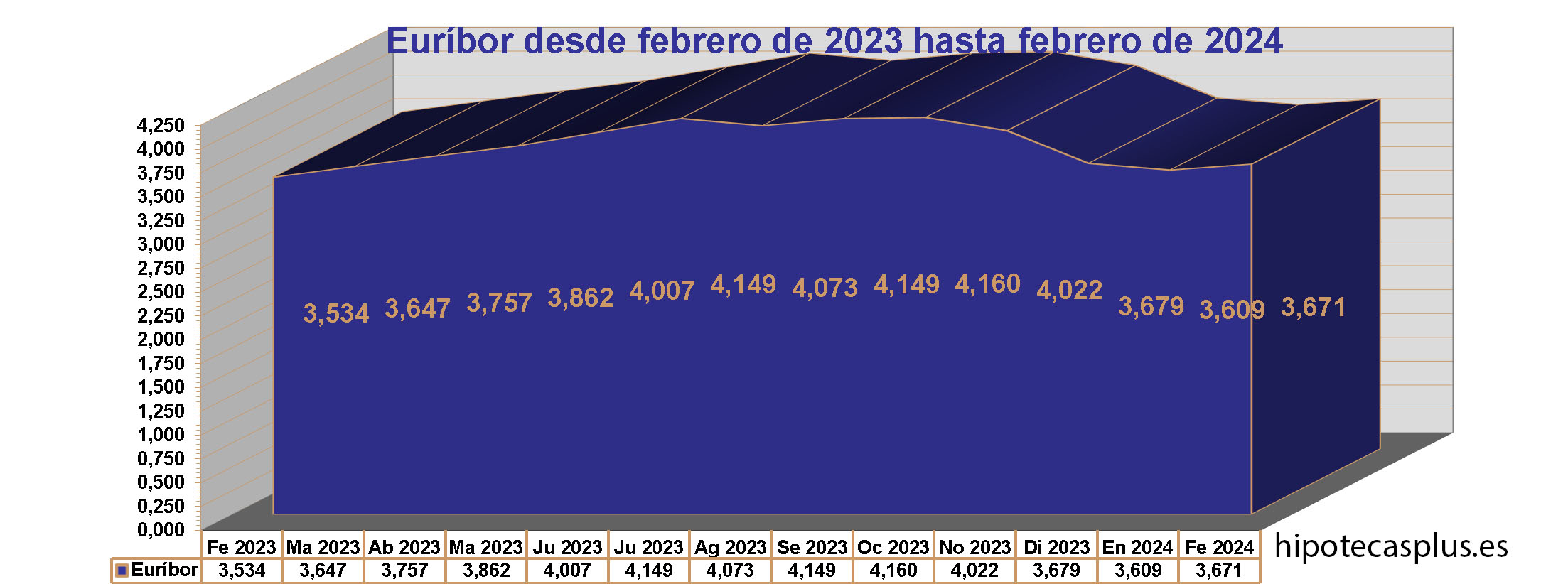

In this way, the daily values ??of the 12-month Euribor during the month of February have been characterized by daily increases. If we start the month with the daily value of 3.505, we end it with 3.749. This daily value is higher than the mortgage Euribor of February, so March will also end with another increase in the Euribor, unless the forecasts of interest rate cuts by central banks are revitalized.

Fear of stalling disinflation

Right now, economic policymakers want to be very cautious. They believe that triggering hasty or premature interest rate cuts could cause the disinflation process, which has been so difficult to set in motion, to come to a halt.

They are going to postpone interest rate cuts for later, and this has led to the Euribor ending February with an increase.

Current Euribor

In the following table, we observe the rise of the Euribor in February compared to the value of the previous month. We also notice that the value of February 2024 is higher than the value of February 2023, so mortgages that are annually reviewed with the February value will become more expensive. However, the current Euribor is higher than it was six months ago, so mortgages that are reviewed semi-annually will become cheaper.

The current Euribor data is as follows:

- A month-on-month increase of 62 thousandths.

- An annual increase of 0.107 points, leading to an increase in the monthly installment of mortgages that are annually reviewed with the February data.

- A semi-annual decrease of 402 thousandths, resulting in a reduction in variable-rate mortgages that are semi-annually reviewed with the new Euribor value.

The analysis department of Bankinter maintains its forecasts. This means it still sees the Euribor following a downward path, which will lead it to approach 3% during 2024 and to fall below that 3% in 2025. Good news for mortgage holders.

Changes in mortgages according to the evolution of the Euribor

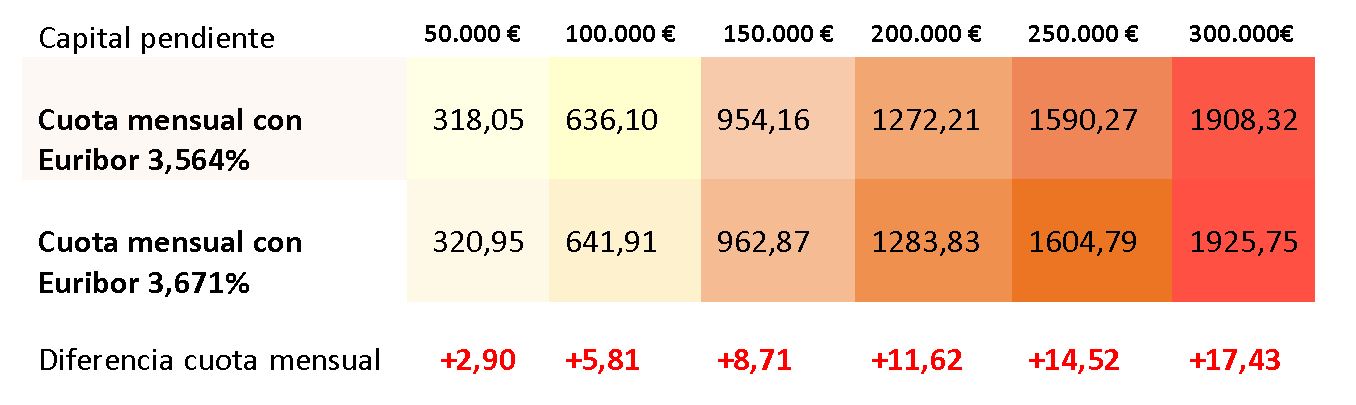

Next, we present how mortgages are affected by the new Euribor data. We take as reference the Euribor of February 2023, which was 3.564%, and the Euribor of February 2024, which has remained at 3.671%.

The previous mortgages all have a remaining term of 20 years and a spread over the Euribor of 1%.

We can see that the increases in mortgage payments are very insignificant. A mortgage of €150,000 increases by less than €10, and another with a larger debt, of €300,000, increases by less than €20.

A mortgage with an outstanding balance of €100,000 with a remaining term of 20 years and an interest rate of Euribor + 1% spread, will see its monthly payment rise from €636.10 to €641.91 with the new Euribor value. This represents a monthly increase of €5.81. All the above data are approximate.

The Euribor has not abandoned its downward trend

Although the Euribor has risen in February 2024 compared to the previous month, we do not anticipate that we are on an upward trend.

The index has recovered from the decline in January, but there is no expectation to suggest that the Euribor has now shifted to a new upward trend.

What has happened is that there was too much optimism about future interest rate cuts, which are likely to be delayed a little longer than expected. Experts predict a Euribor close to 3% for 2024, possibly even lower in 2025.