How to save on the amortization of your mortgage in Spain

15 November, 2023 | M Aparicio

Last Updated on 2 years ago by Antonio Beltrán

When you sign a mortgage with a bank, you usually establish a long-term relationship with the entity. It is many years during which you will have to allocate a significant part of your income to the payment of the monthly installment. And throughout all that long time, your personal finances will surely experience ups and downs. From Hipotecas Plus, we are going to conduct a thorough study on how to save on the amortization of your mortgage.

It’s hard to predict whether your financial situation will be good or bad in the medium to long term, which is why it’s interesting that you might be able to get rid of your mortgage ahead of time or reduce your monthly payment for it.

It’s important for you to know that there is a significant tool to lighten your mortgage debt, and to finish paying it off earlier than initially stipulated or to reduce the monthly installment you pay for it. If you opt to reduce the installment, you will have a larger portion of your income free to use for other expenses or needs, or simply to save.

This powerful tool is called partial mortgage amortization. If you pay off the entire mortgage, we will simply call it mortgage amortization.

We are going to approach the study of how to save on the amortization of your mortgage from three aspects, and we express each of them with a question:

• Saving on mortgage amortization through the type of amortization: How do you save more on amortization, by reducing the installment or the term?

• Saving on mortgage amortization depending on the interest rate: When do you save more money on amortization; with high or low-interest rates?

• Tax benefits thanks to mortgage amortization: How can I get greater tax advantages on the amortization of my mortgage?

Partial Mortgage Amortization

Partial early amortization of a mortgage can be a powerful tool for financial savings. When you have extra money, you can use it to reduce your mortgage debt, and in doing so, you will experience two significant benefits: saving on interest and gaining tax advantages.

Interest savings will occur because owing less money will always result in lower interest costs. As a partial amortization, you can choose between reducing the term or reducing the installment.

Choosing between reducing the installment or the term

When you opt for an early partial repayment, the financial institution will offer you two options: reduce the monthly installment or shorten the term of your mortgage. Each choice has its advantages:

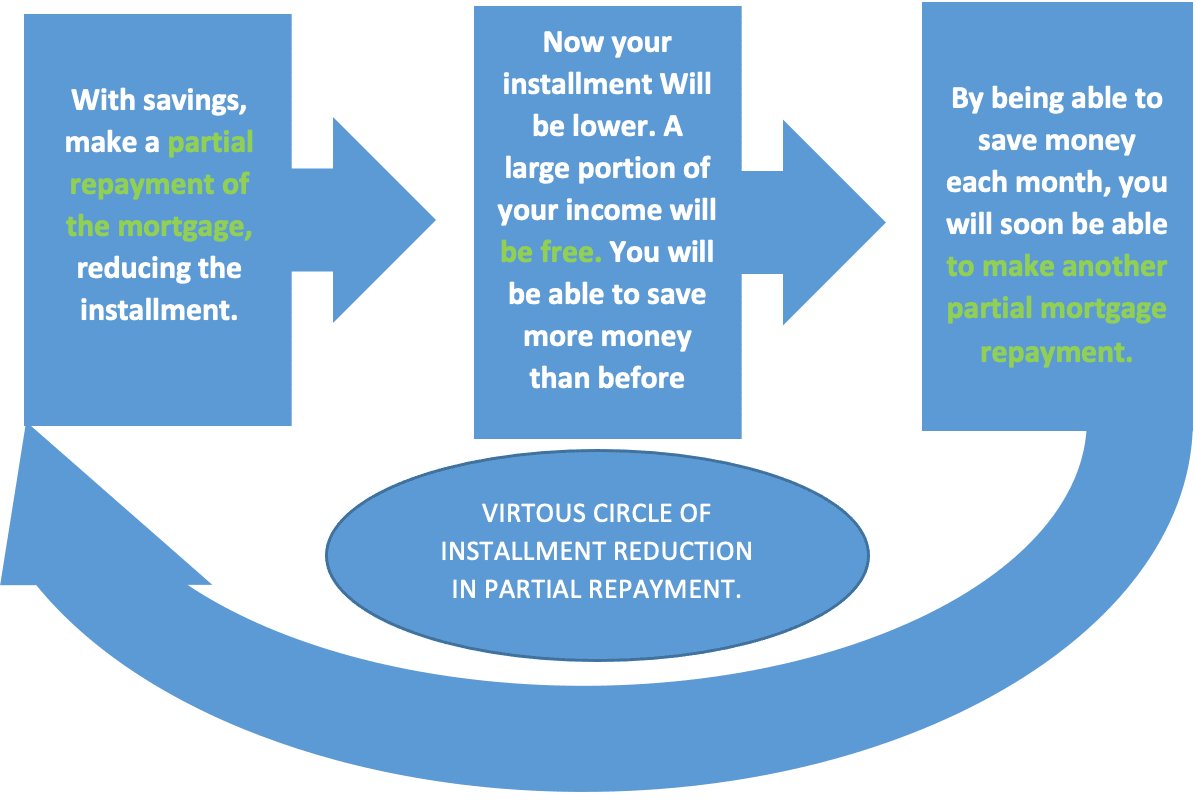

• Reducing the Installment: By reducing the installment, you will ease your monthly financial burden. This means you will pay a smaller amount each month, which can be helpful if you are looking for more liquidity in your budget. Use this option to reduce the installment if you need more money to meet your day-to-day needs.

Furthermore, having more monthly income allows you to save if your economy permits it, and thus you can more quickly approach another partial repayment of the mortgage. This way, you can enter a virtuous circle where you can finish your mortgage much faster than expected.

We could represent this virtuous circle as follows:

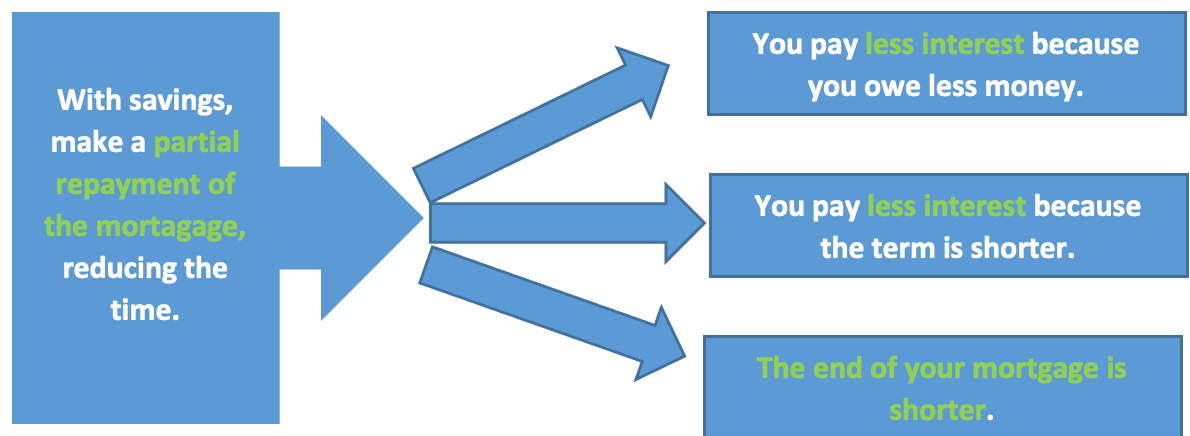

• Reducing the Term: By choosing to reduce the term, you will keep the monthly installment unchanged, but you will decrease the number of years left to pay off your mortgage. This leads to significant long-term interest savings and allows you to be debt-free earlier.

The greatest interest savings occur in the partial repayment of the mortgage by opting for the reduction of the term, as there is a maxim that states, the longer the term of the debt, the higher the interest to be paid on the borrowed money.

Thus, by choosing to reduce the time in the partial repayment of the mortgage, you obtain a multiplying effect of savings and advantages: on one hand, you reduce your debt with the extraordinary contribution, which in itself means paying less interest. But to this reduction of interest, resulting from owing less money, is added the reduction of more interest by shortening the term of the mortgage debt. To this double advantage, we add a third: the end of the mortgage is closer.

This multiplying effect of advantages when reducing the term of the debt in mortgage repayment could be represented as follows:

What is Amortization in a Mortgage?

It’s important to understand the concept of amortization in the context of a mortgage. When a financial institution grants a mortgage loan, the borrowed money is not free. In addition to interest, you must gradually return the entire borrowed amount, which is known as capital amortization. Each monthly payment you make to the bank for your mortgage consists of two components: a portion to pay the interest and another for the amortization of the capital.

Early Partial Amortization: The Saving Strategy

As we have already seen, early partial amortization involves making an extra payment on your mortgage before the due date. This approach offers two fundamental advantages: