The Euribor falls in November to 4.022%

1 December, 2023 | Antonio Beltrán

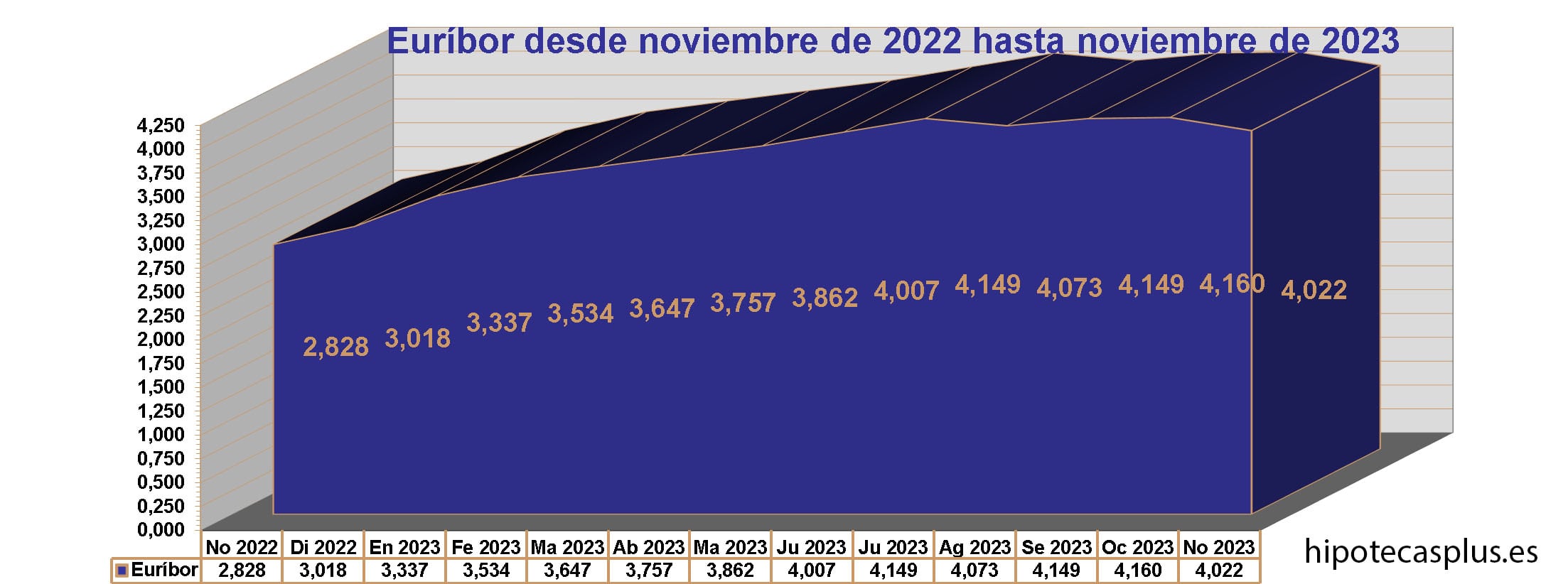

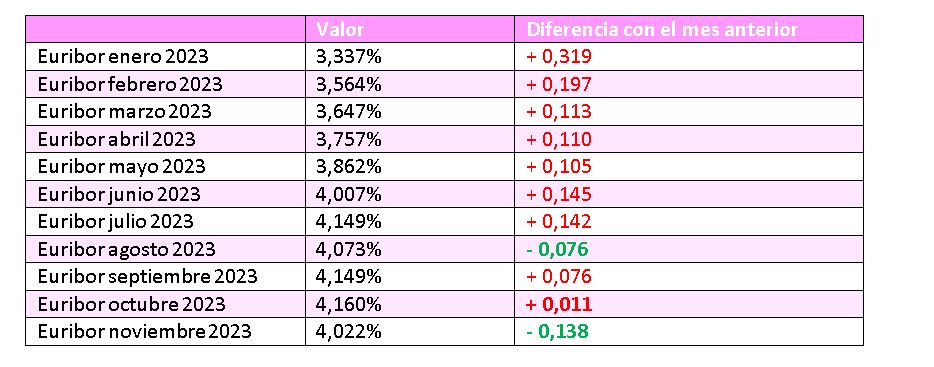

The Euribor has significantly decreased in November 2023, moving from 4.160% in October to 4.022%. This is a significant drop, especially considering that, except for the decrease in August, the Euribor had accumulated 19 consecutive rises and had risen again in September and October.

These 19 rises took the Euribor from below 0% to over 4% in record time. Never before had the Euribor risen so much in such a short period.

However, now in November, the Euribor is falling, and what is hopeful is that even though the European Central Bank (ECB) still does not see the idea of lowering interest rates as imminent, the index is about to lose the 4% mark.

In fact, during the month of November, the 12-month Euribor, which is used to calculate the monthly mortgage Euribor, has indicated several daily values below the psychological barrier of 4%. We see the light at the end of the tunnel. As we predicted at Hipotecas Plus last month, the Euribor has fallen in November and it could be the start of a downward trend for the index.

Messages coming from the ECB

Although the ECB continues to say repeatedly that victory against inflation cannot yet be declared, the fact is that in October it was already decided not to raise interest rates.

The next monetary meeting of the ECB is on December 14th, and given the behavior of the interbank market, with a clearly retreating Euribor, a rate hike seems completely ruled out.

Rather, we should already be thinking about when the first interest rate cut will arrive, even though Christine Lagarde, president of the ECB, tries to maintain a difficult balance in her speech, in the sense that there is no longer a desire to raise interest rates, but also not to lower them, emphasizing keeping them at their current level for a sufficiently long period. However, speeches are gradually adapting to the circumstances, and perhaps that ‘sufficiently long’ time will take on a shorter nuance in her upcoming statements.

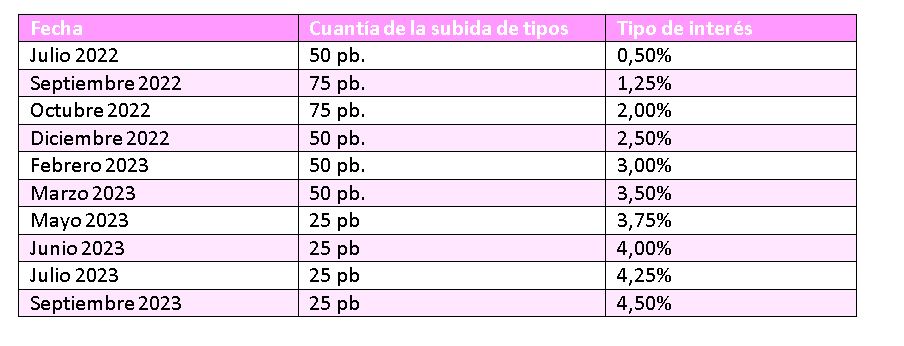

Here we show you the table of the 10 hikes that the ECB has applied to the European economy. They are overly forceful and all consecutive.

Never in the history of the Euro have interest rates been raised so much in such a short period of time, and therefore the Euribor emerged strongly from the negative zone, surpassing 0% and rising above 4%.

In November, we see the second fall of the Euribor within the last 4 months, and we can consider its bullish run and rapid rise to be over. We will consider the value of November as a turning point.

As we can see in the previous table, the November decline is more pronounced than that of August. Another sign of hope.

Euribor Forecasts for 2023, 2024, and 2025

The analysis department of Bankinter forecasts a value of 4.10% for 2023. We might end the year below 4%. In fact, the last two daily values of the 12-month Euribor have been 3.983% (November 29) and 3.926% (November 30).

For 2024, it already foresees a fall in the Euribor, though not too sharp, indicating a central value of 3.90% and for 2025, 3.40%.

But individuals and families with mortgages, rather than knowing the values that analysts and experts predict for the Euribor, want to know when the first reductions in mortgage rates will be experienced. This question leads us to the next point.

When Will Mortgages Become Cheaper

For mortgages to become cheaper, it is necessary that the current Euribor value is lower than the Euribor value at the time of the last mortgage review.

That is, if, for example, our mortgage is reviewed once a year and it is reviewed with the value of the index this month, the current Euribor value has to be lower than the Euribor value from a year ago for the monthly mortgage payment to decrease. If our mortgage is reviewed every 6 months and the review is due with the current index value, the current Euribor must be lower than the one from 6 months ago. And, when can this circumstance occur?

If we look at the Euribor chart, we can realize that the month when this situation might occur is in June 2024, since it was in June 2023 when the Euribor surpassed 4%, and if we are heading towards losing the 4%, in June mortgages can start to lower their payments in the corresponding reviews.

This might occur one or two months earlier, if the ECB applies or at least announces a closer reduction in interest rates.

The Most Current Euribor

Returning to the current situation, we will provide the data indicating the current Euribor. We find ourselves with

• A monthly decrease of 138 thousandths.

• An annual increase of 1.194 points.

• A semi-annual increase of 0.160 points.

• An accumulated annual increase of 1.004 points (from the value of December 2022).

What causes the increase in mortgage costs are the semi-annual and annual rate hikes. With the above data, we can see that for those whose mortgages are reviewed every six months, the mortgage will become more expensive, but only slightly. However, for those whose mortgage is reviewed once a year, their mortgage payment will increase. Almost 1.2% more in interest rate.

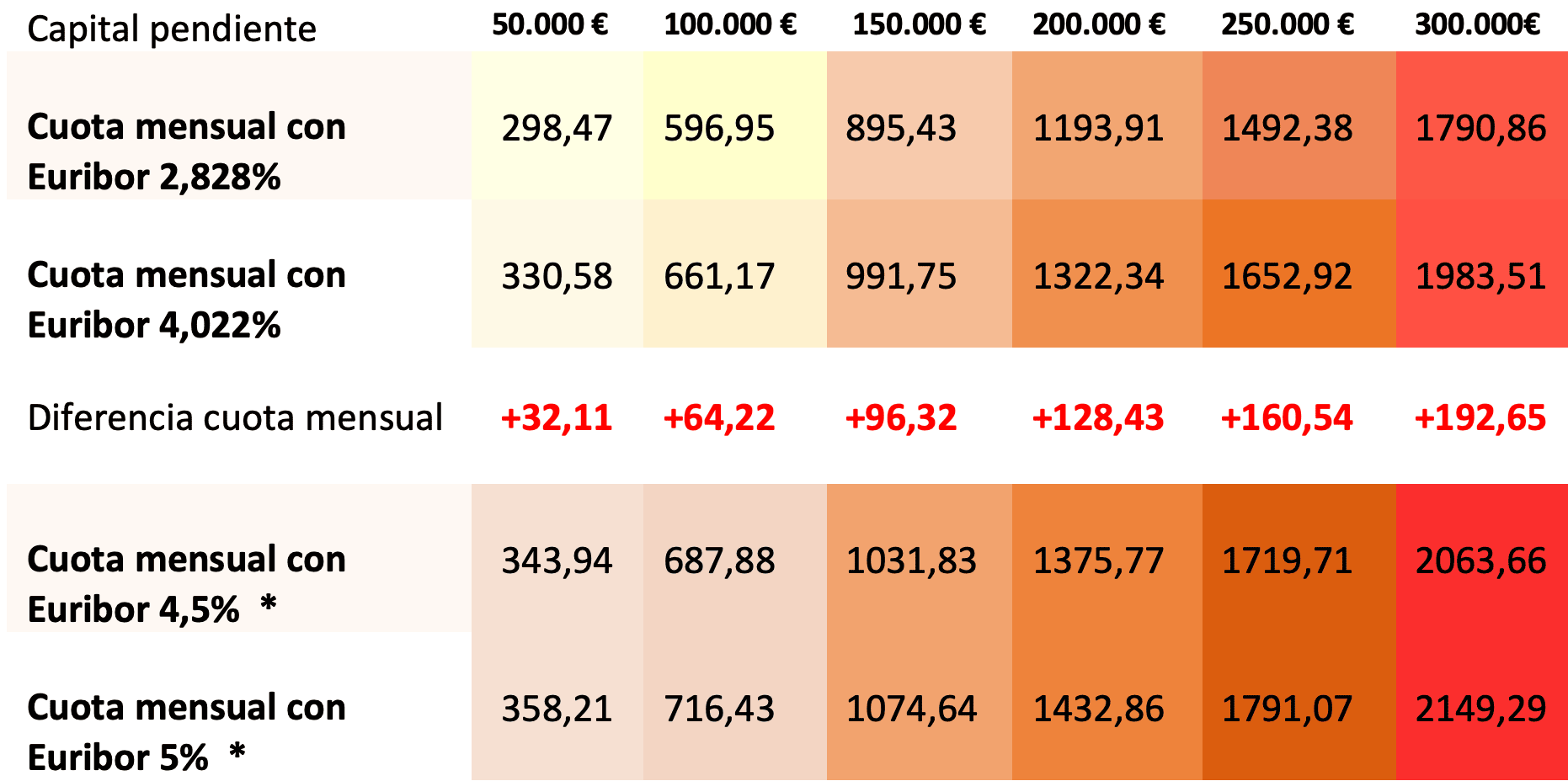

Let’s see this more precisely with our classic table of mortgage examples.

Examples of your mortgages and how they vary according to the evolution of the Euribor

Here we show you 6 example mortgages with outstanding capital ranging from 50,000 euros to 300,000. They have a remaining term of 20 years and a spread over the Euribor of 1%.

The first row indicates the mortgage payments with the Euribor of November 2022.

The second row shows what the mortgage would be according to the value of the Euribor of November 2023.

The middle row indicates the increases that the mortgage payments will experience with the new value of the Euribor.

The penultimate and last row show what the mortgage payment would be if the Euribor rose to 4.5% and 5%.

*These are not real data. According to the current trend of the Euribor, we will not reach those values.

A mortgage with an outstanding capital of €100,000, a remaining term of 20 years, and an interest rate of Euribor + 1% spread, will move from a monthly installment of €596.95 to €661.17 with the new Euribor value. This means a monthly increase in the installment of €64.22. All the above data are approximate.

The Euribor falls and has likely shown the start of its downward trend.

The ECB did not raise interest rates in October and is almost certain not to do so in December. However, even though its president indicates that they want to keep interest rates as they are for a sufficiently long time, analysts already predict a lower Euribor for 2024 and even lower for 2025. We have overcome a tough stage, and we are now entering a period of calm. Sooner rather than later, we will see how our mortgages reflect lower installments than the current ones.