The Euribor fell to 3.703% in April 2024.

1 May, 2024 | Antonio Beltrán

The Euribor has fallen to 3.703% in April. Although it’s a slight monthly decrease from March’s rate of 3.718%, the most significant aspect is that variable-rate mortgages reviewed annually from April’s data will experience their first drop in monthly payments.

This reduction in mortgage payments upon annual reviews is very important because, for over two years, only increases in monthly mortgage payments had been experienced in the annual reviews.

This is the case because exactly one year ago, in April 2023, the Euribor was higher than it is currently. The Euribor value last April was 3.757%, and this April it has decreased to 3.703%; thus, we are looking at an interannual cut of 54 basis points, which will reduce mortgage payments.

This is excellent news for citizens with variable-rate mortgages who have endured increases in their payments for more than two years, many of which have been substantial and thus very burdensome for many individuals and families.

We are already seeing reductions in mortgages, and as we predicted at Hipotecas Plus during the toughest months of rapid Euribor increases, any index, value, indicator, or rate that experiences a significant rise in a short period is full of volatility and will soon see falls, as is already occurring.

The Euribor should fall much further

However, the decrease in the Euribor has not yet been significant enough, especially considering that during 2022 and 2023, the Euribor rose dramatically. The Euribor had never risen so much in such a short time.

The economic imbalances caused by the Covid-19 pandemic and the conflict in Ukraine led to rampant inflation. The European Central Bank (ECB) responded with significant interest rate increases, which caused a rapid rise in the Euribor over the last two years, and many individuals and families saw substantial increases in their mortgage costs.

For these reasons, we say that although the Euribor is already receding, it needs to decrease much more, because its increases were excessive for such a short period.

Why the Euribor Isn’t Falling Faster

The Euribor will not decrease more rapidly but will instead remain in a state of stasis, alternating minor increases with similarly insignificant decreases until the ECB decides to lower the cost of money, that is, to reduce the current interest rates set at 4.5%.

Under the presidency of Christine Lagarde, the ECB is increasingly aware that interest rates must soon be lowered. Once rate cuts begin, the Euribor will accelerate its decline.

Inflation, meaning the prices of consumer goods, has clearly decreased, and the economy of the Eurozone is beginning to deteriorate, or at least, it is clearly cooling down. These are clear indicators that the cost of money cannot remain so high, or in other words, the interest rates cannot be maintained at 4.5% for much longer.

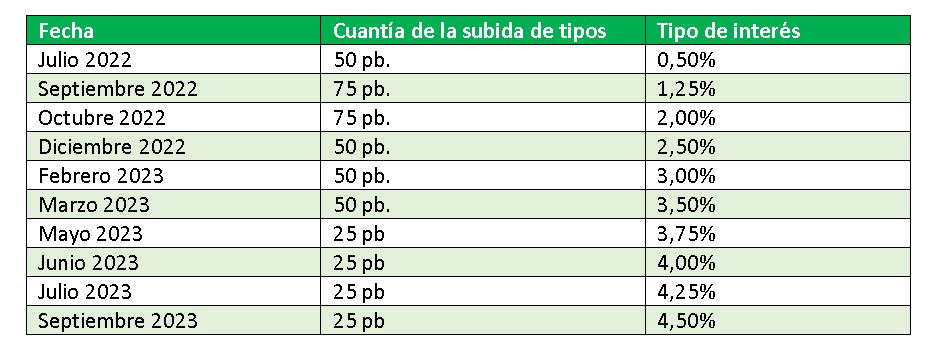

This is the table showing the 10 consecutive increases applied by the ECB during 2022 and 2023, which significantly drove the Euribor higher. Soon, we will be able to add new lines to the table, but this time they will be of rate cuts.

The next monetary policy meeting of the ECB’s Governing Council is scheduled for June 6, 2024. There is a strong likelihood that at this meeting, the first interest rate cut will be agreed upon. Such rate cuts are the driving force for a stronger retreat in the Euribor and for reducing monthly payments on variable-rate mortgages.

Current Euribor Data

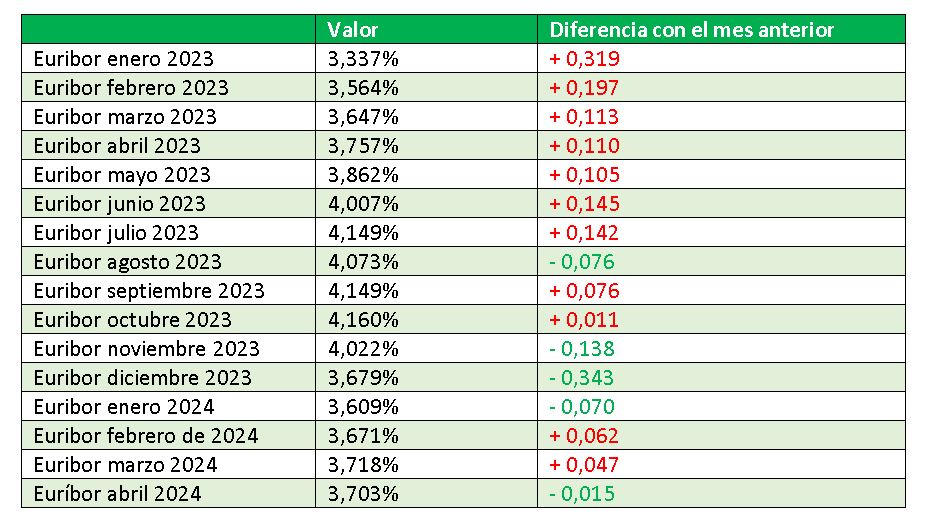

Here we show you the Euribor values from January 2023 to the present and how they have risen or fallen compared to the previous month.

In April 2024, we encountered a decrease after two consecutive increases.

The current Euribor data are as follows:

- A monthly decrease of less than 15 basis points.

- An annual drop of 0.054 points. As this is an annual reduction, mortgage payments will decrease when reviewed annually with the new data from April 2024.

- A semi-annual decrease of 457 basis points, which will lead to a reduction in variable-rate mortgages that are reviewed every six months.

Euribor Forecasts for 2024 and 2025

The forecasts from Bankinter’s analysis department continue to maintain the perspective that the ECB will lower interest rates in 2024 and also during 2025.

For this reason, they predict the Euribor for 2024 and 2025 will follow a downward trend that will bring it closer to 3% during this year and below that 3% in 2025.

Specifically, it estimates a central value of 3.25% and 2.75% for 2024 and 2025, respectively.

Mortgages Following the Current Evolution of the Euribor

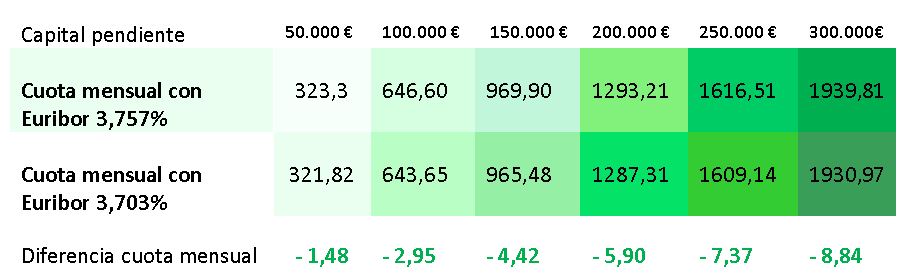

In the following table, we can now register green data indicating reductions in mortgages, after many months of showing red data due to increases in monthly payments.

For now, the reductions in monthly payments are minor, but it is great news that the first reductions in variable-rate mortgages are already being given.

In these examples of 6 mortgages ranging from 50,000 € to 300,000 € in outstanding capital, we observe that the greater the remaining capital, the larger the reduction that occurs.

A mortgage with an outstanding capital of 100,000 €, with a remaining term of 20 years and an interest rate of Euribor + 1% spread, will see its monthly payment change from 646.60 € to 643.65 € with the new Euribor rate. This translates into a monthly reduction of 2.95 €. All the above data are approximate.

At last, the reductions in mortgage payments have arrived

We are bidding farewell this month to the increases in mortgage payments.

As we indicated in our Euribor article last month, April could probably be the first month in which reductions in mortgage payments occur. And so it has been. This is very good news for citizens with a mortgage.