The Euribor slightly rises in October to 4.160%

1 November, 2023 | Antonio Beltrán

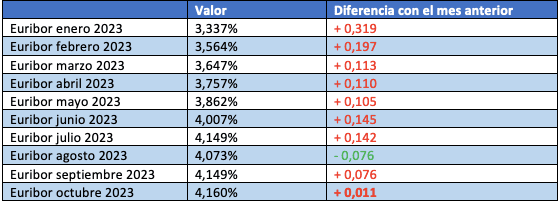

The Euribor has risen again in October, but very slightly compared to September. Thus, if in September it was at 4.149%, now in October it stands at 4.160%.

Despite a new month-to-month increase, there are several indicators suggesting that the Euribor may be beginning its decline. We must remember that the 12-month Euribor started October with values close to, and even above, 4.2%, yet the month ends with values approaching 4%.

It’s important to recall that the monthly Euribor rate, which is used to adjust variable interest mortgages linked to this index, is formed from the daily values of the 12-month Euribor.

The ECB has not raised interest rates in October

At the meeting of the Governing Council of the European Central Bank (ECB) on October 26, 2023, it was decided not to raise interest rates, leaving them at 4.5%. In this way, they have remained as they were after the last hike undertaken by the European issuing institute in September 2023.

Before July 2022, just over a year ago, interest rates were at 0%, and in September 2023, they reached 4.5% after applying 10 consecutive increases, some of them with a significant rise of 75 basis points.

There had never been so many interest rate hikes in such a short time. And this is the cause of the Euribor experiencing such a steep rise, also never seen before.

This is how the news was published by the Bank of Spain: The ECB keeps interest rates unchanged in October.

A Breather and Start of Calm for Mortgage Holders

The monetary institution of Europe has left the price of money at 4.5%, thereby providing relief to those with mortgages. Mortgages undergoing revision will still experience price increases, as the Euribor is still above the index values from 3, 6, or 12 months ago, but these increases in monthly payments are soon to end.

There are more than 5 million families or households with a variable-rate mortgage, and all signs indicate that they will feel the relief of the Euribor having reached its peak.

Christine Lagarde seems satisfied with her fight against the cost of living, and in her press conference, she delivered some hopeful messages indicating that inflation sharply fell to 4.3% in September, and that the actions taken so far are strongly translating into financing conditions, in the sense that demand is increasingly being curbed, thereby helping to bring down inflation.

Euribor Forecasts 2023, 2024, and 2025

As we draw closer to the end of 2023, the potential fall of the Euribor appears increasingly imminent.

In this way, for 2023, the Analysis Department of Bankinter forecasts a central Euribor rate of 4.10%, figures very close to where we currently stand. For 2024, this central rate will be 3.90% and for 2025, 3.40%.

This fall in the Euribor can only be forecasted by seeing it feasible that inflation will soon settle at levels acceptable to the ECB, which could then order a decrease in interest rates.

Current Euribor Data

Here are the current Euribor figures:

- An inter-month increase of 11 basis points.

- An inter-annual rise of 1.531 percentage points.

- An annual cumulative increase of 1.142 percentage points.

The significant difference between the current Euribor value: 4.160% and the Euribor value from a year ago: 2.629%, will lead to significant increases in the monthly payments of variable-rate mortgages that are reviewed annually based on October’s figures.

Examples of your mortgages and how they vary according to the evolution of the Euribor

We show you below a table with six example mortgages, whose outstanding capitals range from 50.000 € to 300.000 €. The remaining term is 20 years and the spread over the Euribor is 1%.

The increase in mortgage costs is more pronounced as the outstanding capital is larger, that is, the monthly installment increases more as the amount of money owed to the bank for the mortgage loan is greater.

The first row refers to how the mortgage payments stood with the value of the Euribor a year ago.

The second row refers to what the mortgage amounts to according to the current value of the Euribor.

The middle row, with no background color, pertains to the difference between the monthly installment from a year ago and the current mortgage installment based on the Euribor value from October 2023.

The second-to-last and last row refer to what the mortgage installment would be if the Euribor rose to 4.5% and 5% respectively.

*These are not real figures. The Euribor has not reached these values, and according to the news coming in, it seems unlikely to do so.

A mortgage with an outstanding capital of €100,000, with a remaining term of 20 years, and with an interest rate of Euribor + 1% spread, will go from a monthly payment of 586.61 € to a new payment of 668.82 € with the new value of the Euribor. This represents a monthly increase of 82.21 € in the payment. All the above figures are approximate.

The Euribor is getting closer to a downward trend

Inflation is decreasing, the ECB has stopped ordering new interest rate hikes, and in the daily values of the 12-month Euribor of the last few days, we already observe a significant retreat in the numbers.

Most likely, November 2023 will end with a Euribor value lower than that of October 2023, and it is possible that November will be the first month of a downward trend for the Euribor. If the forecasts are met, in 2024 and 2025 we will start to see the first reductions in mortgages. This is what is expected and what is needed: peace of mind for citizens with mortgages.