Euribor Drops Again, Reaches 3.650% in June 2024

1 July, 2024 | Antonio Beltrán

The Euribor continues its downward trend, falling for the third consecutive month to 3.650% in June 2024.

These are good figures as we move further away from the psychological barrier of 4%, and considering that just a year ago, the Euribor was on an upward trend, the decrease in mortgage payments is growing each month.

Thus, variable-rate mortgages that are reviewed from June onwards will see a greater reduction than if they had been reviewed the previous month.

Will the Downward Trend for Euribor Continue?

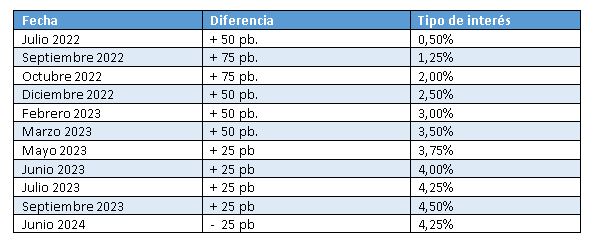

The Euribor is currently falling because on June 6, the European Central Bank (ECB) ordered the first rate cut in eight years. This came after 10 consecutive and often significant hikes during 2022 and 2023.

This first rate cut was 25 basis points, bringing them to 4.25%. Initially, there was talk of a gradual reduction in interest rates that would imply a continuous fall in Euribor during 2024 and 2025.

However, this optimism has cooled, and it is now less likely that there will be several interest rate cuts by the ECB. The next monetary policy meeting of the ECB’s Governing Council will take place in Frankfurt on July 18. We will see what happens, especially if another cut is applied or rates are kept at 4.25%.

For now, we can add a new line corresponding to the 25 basis point cut applied on June 6. If another cut occurs on July 18, we will insert a new line in our interest rate table.

Bankinter’s Analysis Department Changes Its Forecasts

The Analysis Department of Bankinter has updated its forecasts, and unfortunately, the changes have been to raise its predictions regarding the Euribor.

Last month, it predicted that we would reach 3.25% in 2024 and 2.75% in 2025; now it indicates 3.5% for 2024 and 3% for 2025. What is truly surprising is that it also provides a forecast for 2026 and raises it! Specifically, Bankinter thinks the Euribor will rise to 3.25% as a central value after falling to 3% in 2025.

We must emphasize that these are forecasts and therefore may not be fulfilled. Additionally, analysts are prone to making changes quite frequently.

So, we should take the information offered by these forecasts with caution. It is better to keep in mind that for now, the Euribor is falling and will likely continue to do so during 2024 and 2025.

Current Euribor

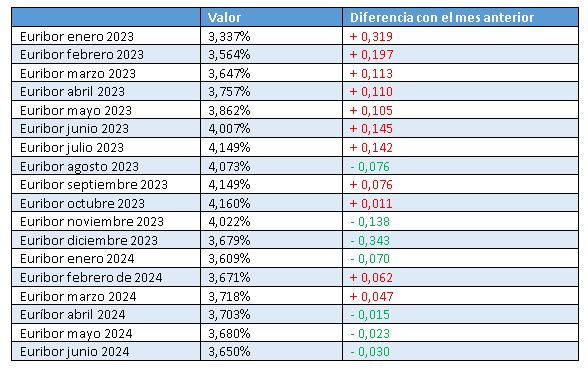

Since forecasts are merely hypothetical data that may or may not occur, let’s look at the current Euribor data and how they affect mortgages. With the new Euribor value at 3.650%, we see the following variations:

- A monthly decrease of 30 thousandths.

- An annual decrease of 357 thousandths. Recall that a year ago, in June 2023, the Euribor surpassed the 4% barrier and stood at 4.007%, while now it has dropped to 3.650%. This is an excellent figure that will reduce the monthly payment of mortgages reviewed annually from the June data.

- A six-month decrease of 0.029 points. Mortgages reviewed semi-annually will also become cheaper, but only slightly. Six months ago, in December 2023, the Euribor was at 3.679%, a value similar to the current one.

Here is the table showing the Euribor evolution since 2023. As we can see, with June’s decline, we have now had three consecutive drops:

Mortgages Following the Current Euribor Evolution

We present a new table with six possible mortgages ranging from 50,000 to 300,000 euros of outstanding capital. We must keep in mind that the mortgage review is based on the remaining term and the outstanding capital, not the initial loan amount.

The less capital we owe over time, the less variation in the monthly payment we will experience with Euribor changes.

The bottom row indicates the amount of reduction in the monthly mortgage payment from the annual review with the June Euribor data.

If we review last month’s table, we see that the reduction practically doubles, or in other words, increases by 100% compared to the previous month, which is good news for citizens with variable-rate mortgages reviewed with this month’s Euribor data.

With these data, a variable-rate mortgage reviewed annually with the June Euribor data, with an outstanding capital of 100,000 euros, a remaining term of 20 years, and a 1% differential over the Euribor, the monthly payment will decrease by approximately 19.08 euros per month. This translates to an approximate annual saving of 228.96 euros.

Continued Reductions in Mortgages

The good news is that mortgages continue to become cheaper, improving the economies of many people and families month by month after very difficult years with significant increases in monthly payments.

Although analysts do not currently predict sharp declines and even forecast an increase in 2026 compared to 2025, we should remain optimistic as we move further away from a 4% Euribor. Even if the increase occurs in 2026, the Euribor will remain close to 3%.