Euribor on the Decline: December 2023 Closes at 3.679%

31 December, 2023 | Antonio Beltrán

Last Updated on 2 years ago by Antonio Beltrán

The Euribor has dropped significantly in December 2023, reaching 3.679%. This marks the second consecutive decline in the Euribor and the third drop in the last five months. Of these three decreases, the one in December is the most significant.

At Hipotecas Plus, we had already warned that the Euribor had reached its peak, and we were facing a turning point. We also mentioned for several months that any index, rate, value, or indicator that experiences a spectacular rise in a short period can only expect a considerable fall in the near future.

Good News Arrives

Finally, the time has come to bring good news to individuals and families with mortgages. We are finally at the end of a tough period for mortgage holders in the years 2022 and 2023. And we are now in a position to indicate that mortgages that are reviewed semi-annually, that is, every 6 months, will now experience their first reduction.

Therefore, the doors are now open for reductions in mortgages that will be reviewed with the new Euribor data. This is because the current mortgage Euribor, as of December, stands at 3.679%, which is lower than the Euribor from 6 months ago, which was higher, specifically, the Euribor in June 2023 was 4.007%.

Mortgages that are reviewed annually with the December Euribor data will still experience an increase. One year ago, in December 2022, the Euribor closed the year at 3.018%, so there will be an increase for these mortgages. However, there is a very promising future for families and individuals with mortgages.

Euribor Accelerates Its Decline

The spectacular drop in the Euribor over this past month has advanced the timeline for when all variable-rate mortgages will begin to lower. Most likely, in March, we will already be talking about reductions in annually reviewed variable-rate mortgages.

It may even be in February that we indicate reductions in the installments of all variable-rate mortgages. This is because the latest daily values of the 12-month Euribor, which are the ones used to calculate the mortgage Euribor, already showed values similar to those of February 2023 in the last days of December.

Specifically, on December 29th, we saw a 12-month Euribor at 3.513%, while the Euribor for February 2023 was 3.534%, which is slightly higher.

The Euribor’s Splendid Fall

The interbank market moves very swiftly, and these significant retreats in the Euribor have their reasons. The end of the interest rate hikes arrived three months ago, and now in the financial landscape, we see interest rate reductions looming, and they won’t be minor.

2024 is very likely to come with significant changes in the monetary policies of Central Banks.

Interest rate cuts are on the horizon, as both the Federal Reserve (Fed), the Bank of England (BoE), and our European Central Bank (ECB) are well aware that the economy cannot be strangled, or at the very least, cooled down as severely as it was during 2022 and 2023.

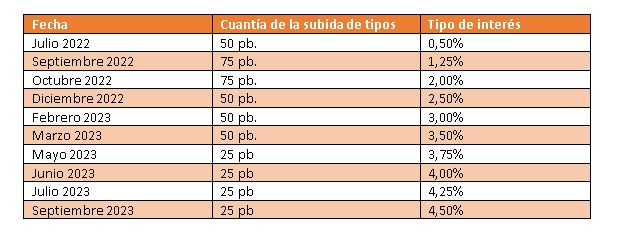

These are the 10 consecutive rate hikes that the ECB has implemented in the eurozone economy over the past two years:

Mid-2022 was when apprehension arose about controlling rampant inflation, leading to robust interest rate hikes.

The tough monetary medicine has been administered in progressively milder doses throughout 2023. However, the result has been an increase in interest rates from 0% to 4.50%, which inevitably pushed the Euribor upwards, reaching values above 4% and significantly increasing variable-rate mortgages.

Significant Interest Rate Reductions on the Horizon

We expect to soon add lines of interest rate reductions to the previous table for 2024. Analysts and experts are indicating this direction.

So much so that T. Rowe Price, a highly regarded investment management company, has suggested that the ECB will cut interest rates by 150 to 250 basis points. This would bring them down to between 2% and 3%, which would be excellent news for individuals with mortgages tied to the Euribor. The interbank market is already factoring in the very likely interest rate cuts that are anticipated in the near economic landscape.

Current Euribor

Happily, we can add a new downward trend line to our 2023 Euribor table, and thus, the spectacular drop in December promises a more than hopeful 2024.

As we mentioned last month, we observed in the previous table that the decline in November was more pronounced than in August. We indicated that this was a sign of hope, and indeed it has been: it was a prediction of a further decline to conclude 2023, with a decrease of 0.343 points in the Euribor value.

Thus, the current Euribor data is as follows:

A month-on-month decrease of 0.343 points. A semi-annual decrease of 328 thousandths. Mortgages that were reviewed semi-annually in June 2023 with a Euribor of 4.007% will be the first ones to experience reductions in their monthly installments with the new Euribor data for December: 3.679%. We will provide an example at the end of the article.

An annual increase of 661 thousandths (The Euribor was at 3.018% a year ago), which this time coincides with the cumulative increase during 2023, i.e., since December 2022.

Euribor Forecasts for 2023, 2024, and 2025

Bankinter’s Analysis Department, in response to the new developments in the macroeconomic landscape and a significant drop in the Euribor in December 2023, has been compelled to revise its Euribor forecasts for 2024 and 2025.

A month ago, it predicted a Euribor rate in 2024 that was below but close to 4%. However, it now places the central value at 3.25%, which means it now sees it close to 3% rather than 4%. Their forecasts are even more optimistic for the Euribor in 2025, as they project it to be below 3%, specifically envisioning a Euribor rate of 2.75%.

In the following table, we summarize their Euribor forecasts:

Examples of Their Mortgages and How They Vary with the Euribor’s Evolution

We will illustrate the increases in different mortgages that are reviewed annually based on the new Euribor data. Finally, we will provide an example of how a sample mortgage that is reviewed semi-annually will be affected, so we can confirm that it will already have its first reduction in the monthly installment.

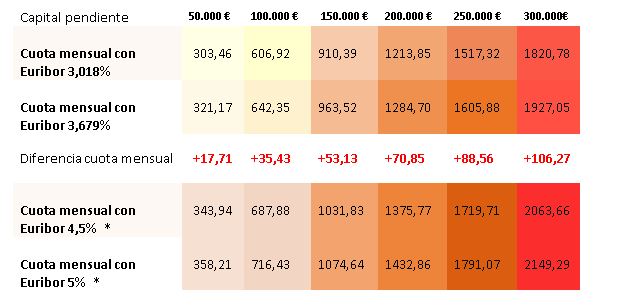

There are 6 example mortgages with outstanding balances ranging from 50,000 euros to 300,000 euros. They have a remaining term of 20 years and a 1% spread over the Euribor.

The first row indicates how the mortgage installments were affected by the Euribor in December 2022.

The second row shows how the mortgage is affected based on the Euribor value in December 2023.

The middle row indicates the increases that the mortgage installments will experience with the new Euribor value.

With the significant drop in the Euribor in December, we can see in the middle row that the increases for mortgages reviewed annually are not excessively significant. Only those mortgages with a large outstanding balance of 300,000€ will see increases surpassing 100 euros. Small mortgages of 50,000 € will only experience an increase below 18€.

The penultimate and last rows show how the mortgage installment would be affected if the Euribor were to rise to 4.5% and 5%. However, the danger has clearly receded, and we are not going to reach those high Euribor values.

*These are not real data. According to the current downward trend of the Euribor, we will not reach those values.

A mortgage with an outstanding balance of 100,000 €, a remaining term of 20 years, and an interest rate of Euribor + 1% differential, will see its monthly installment increase from 606.92€ to 642.35 € with the new Euribor value. This represents a monthly increase of 35.43 €. All the above data are approximate.

The first reductions in mortgages that are reviewed semi-annually

We don’t want to conclude the article without emphasizing the news that we will now see reduced monthly installments for variable-rate mortgages. This applies to those that are reviewed semi-annually with the December Euribor data. The current Euribor is at 3.679%, but six months ago, in June 2023, the Euribor was higher, at 4.007%.

Therefore, a mortgage with a principal of 100,000 €, a remaining term of 20 years, with a one-point differential on the Euribor, and semi-annual review based on the December 2023 Euribor, will see its monthly installment decrease from 660 € to 642 €. This represents a reduction of 18 € per month. These are approximate figures.