How does energy certification influence your mortgage?

3 July, 2024 | M Aparicio

At Hipotecas Plus, we fully understand that buying a home and signing a mortgage are very important decisions for many people and families. Therefore, it is essential to consider various factors and information to make the best possible decision.

One of these factors that we often overlook is the energy certification of the home.

What is energy certification?

Energy certification consists of an official document that details an assessment of the home’s energy efficiency. Like any evaluation, it offers a rating and in this case, it is a letter that can be as follows: A B C D E F G; with A being the most efficient and G the least efficient.

The rating is determined based on two important variables:

- Energy consumption

- Carbon dioxide (CO2) emissions from the home.

This certificate provides a detailed analysis of the energy performance of your home. Undoubtedly, having an efficient energy performance is very important because it will provide significant relief in your monthly expenses and also mean that your property has a higher value.

Influence of energy certification on the mortgage

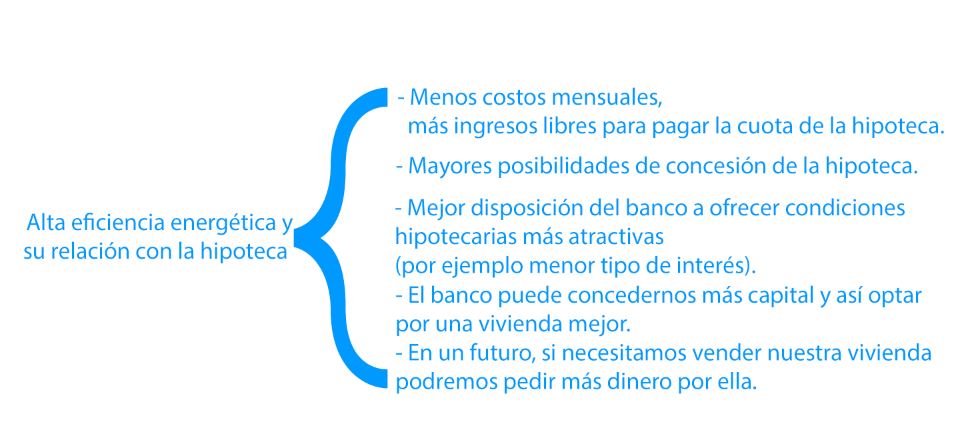

We must consider banks as very rigorous and precise analysts when granting a mortgage. They take into account all possible variables, and if the home you are going to purchase has a high energy rating, they will know in advance that you will have fewer monthly expenses. This directly implies that you will have a greater part of your income free to face the monthly mortgage payment with greater financial ease.

Keep in mind that good energy performance from your property will allow you to save on:

- Heating

- Cooling

- Electricity consumption

- Lower electricity and gas bills. These are more economical maintenance costs that will result in considerable savings in the long run.

In fact, if the home has a high energy certification, this could be a key factor in obtaining mortgage approval. There are financial institutions that will offer you more attractive interest rates if the home presented as collateral has a good energy rating. Banks may also offer subsidies for energy improvements.

In this way, we see that good energy efficiency can mean not only the granting of the mortgage but also that it comes with more attractive conditions such as a lower interest rate.

In other words, having a home with a good energy rating provides advantages from various fronts: we will save on our monthly payments and also save thanks to a cheaper mortgage or with better conditions.

To this, we must add what we have mentioned before: our property will have a greater intrinsic value. If in the future you need to sell your home, you will be able to obtain a higher price for it.

Also, this high energy efficiency of your home can be an important factor when it comes to obtaining a larger amount of money lent, meaning perhaps it will allow you to opt for a more expensive and consequently better home.

We can summarize the relationship between energy rating and mortgage and its advantages with the following scheme:

If your home has a high energy rating, you care for the environment.

People are increasingly aware that our planet needs to be cared for and that we all must do our part. An excellent way to do this is to try to make our home as energy-efficient as possible.

Homes with high energy ratings emit a smaller amount of carbon dioxide into the environment. In many media outlets, we hear about our carbon footprint; with our efficient home, we contribute to making our footprint on the planet much smaller.

More efficient homes equal more comfortable homes.

If we have a home that is energy-efficient, it is very likely that we will also feel greater well-being and comfort living in it. This leads to a better quality of life. This is because these homes have better insulation and better air quality inside.

Also, heating and cooling systems tend to be more effective, making us feel better both in winter and summer, which are the seasons in which we usually use heating and cooling respectively.

Green mortgages

A clear example of everything we have discussed above are green mortgages.

The green mortgage is that mortgage loan that is designed and granted specifically for the purchase, rehabilitation, or construction of homes that meet environmental sustainability and energy efficiency criteria.

These are mortgages with more advantageous conditions such as longer terms or lower interest rates. They are offered by different financial entities with the aim of motivating citizens to purchase homes with high energy ratings, that is, that are highly respectful of the environment.

Other benefits such as cheaper insurances or commissions are also offered.

Green mortgages are also called ecological mortgages, and it is usually required that the energy certificate has an A rating.

What makes a mortgage green or ecological?

The home that is going to be the collateral for the green mortgage must meet a series of conditions that will lead it to have an A rating in its energy certificate.

These conditions are mainly the following:

- Renewable energies must be very present. We are talking about solar panels or wind turbines. These systems allow the home to be as independent as possible from the use of non-renewable energy sources.

- Energy efficiency of appliances. We must not forget that appliances and electrical devices also have their own energy certificate. We must try to ensure they have the letter A or at least the letters B or C. Washers, dryers, freezers, dishwashers, electric ovens, Smart TVs, air conditioning units, and also lamps and bulbs are required to have their corresponding energy certificate. Remember that there are appliances that also incorporate the categories A+ A++ and A+++.

So before purchasing and installing them, it’s better to thoroughly review their energy efficiency rating.

- Having highly efficient heating and hot water cooling systems such as geothermal heat pumps, low-temperature radiators, condensing boilers, solar hot water systems, evaporative coolers, or air conditioners that have Inverter technology.

- Also, use LED lighting systems. It is about installing lighting with low energy consumption.

If these conditions are met, it is very likely that the bank can grant the mortgage loan with the benefits of the green mortgage.

There are public aids such as the Next Generation Funds that have been activated by the European Union and the Government of Spain with the aim of achieving ecological transition. Learn more about them by clicking on the link.

Conclusions

Energy certification has significant value and influence on the mortgage. You can obtain incentives, discounts, subsidies… For example, a longer amortization period, a greater amount of capital granted, a lower interest rate, or public aids from administrations.

Moreover, by acquiring an energy-efficient home, you are contributing to caring for the environment.

On the other hand, your home will have a higher value, so if in the future you need to sell it, you will get more money for it. This amount will add to the savings you have made while living in it due to lower costs in heating, cooling, and cheaper gas and energy bills.