La traducción al inglés de tu texto es:

-

Spain

Interest Rates: Spain offers mortgages at both fixed and variable interest rates. Variable rates are often linked to the Euribor.

Amortization Period: Amortization terms in Spain typically go up to 30 years. LTV: The maximum LTV is generally 80% for residents and 70% for non-residents.

Regulation: The mortgage market in Spain, like the rest of Europe, is regulated by Law 5/2019, of March 15, governing real estate credit contracts.

Costs: Closing costs for a mortgage in Spain include taxes and notary fees.

-

United Kingdom

Interest Rates: In the UK, mortgage rates can be fixed or variable, and some mortgages are base rate variable.

Amortization Period: Typical amortization terms are 25 to 30 years.

LTV: The maximum LTV is generally 95% for first-time buyers and 85% for others.

Regulation: The Financial Conduct Authority (FCA) regulates mortgages in the UK.

Costs: Costs include legal fees, application fees, and possibly a mortgage agreement fee.

-

France

Interest Rates: Mortgage rates in France are mostly fixed-rate.

Amortization Period: The terms are generally 15 to 30 years.

LTV: The maximum LTV is typically 80%.

Regulation: The market is regulated by the Bank of France and the Financial Markets Authority.

Costs: Costs include taxes, notary fees, and real estate agent commissions.

-

Italy

Interest Rates: Italy offers both fixed and variable rates.

Amortization Period: Typical terms are 15 to 30 years.

LTV: The maximum LTV is generally 80%.

Regulation: The Bank of Italy oversees the mortgage market.

Costs: Include taxes, notary fees, and real estate agent fees.

-

Germany

Interest Rates: Mortgage rates are mostly fixed-rate.

Amortization Period: Terms are typically 5 to 30 years.

LTV: The maximum LTV is 80%.

Regulation: The market is regulated by the German Central Bank (Bundesbank).

Costs: Include notary fees and registration expenses.

-

Sweden

Interest Rates: In Sweden, mortgage rates are variable and generally linked to the STIBOR index.

Amortization Period: Terms are generally up to 30 years.

LTV: The maximum LTV is 85%. Regulation: The market is regulated by the Swedish Financial Supervisory Authority.

Costs: Include notary fees and registration charges.

-

Norway

Interest Rates: Mortgage interest rates in Norway are primarily fixed-rate or variable-rate.

Amortization Period: Typical amortization terms are 20 to 30 years.

LTV: The maximum LTV is 85%. Regulation: The market is regulated by the Bank of Norway.

Costs: Include taxes and registration fees.

-

Finland

Interest Rates: Mortgage rates in Finland can be fixed or variable.

Amortization Period: Typical terms are up to 25 years.

LTV: The maximum LTV is 95%. Regulation: The market is regulated by the Finnish Financial Supervisory Authority.

Costs: Include taxes, notary fees, and registration expenses.

-

Ireland

Interest Rates: Ireland offers mortgages at fixed and variable rates.

Amortization Period: The terms of amortization are generally up to 30 years.

LTV: The maximum LTV is usually 80%. Regulation: The Central Bank of Ireland regulates the mortgage market.

Costs: Include taxes and legal fees.

-

Switzerland

Interest Rates: Mortgage rates in Switzerland can be fixed or variable, and variable rates are often linked to the LIBOR.

Amortization Period: Typical terms are 10 to 20 years.

LTV: The maximum LTV is generally 80%.

Regulation: The market is regulated by the Financial Market Supervisory Authority.

Costs: Include notary fees and registration expenses.

These are the key differences in the mortgage markets of the mentioned countries. However, rates and regulations can change over time, so it is important to obtain up-to-date advice when considering a mortgage in any country.

European Mortgage Legislation?

As of today, there is no unified law that regulates mortgage legislation throughout the European Union. Mortgage regulation is the responsibility of the EU member states, meaning each country has its own set of rules and regulations regarding mortgages. However, the European Union has adopted certain directives and regulations that establish minimum standards and protections for consumers in the mortgage sector.

One of the most relevant directives is Directive 2014/17/EU, also known as the European Union Mortgage Credit Directive. This directive sets common rules and standards for mortgage credit contracts in the EU with the goal of protecting consumers and promoting transparency in the mortgage market. However, this directive does not completely harmonize mortgage legislation in all aspects and allows some leeway for member states.

How the Rise in Interest Rates Affects Mortgages in Different European Countries

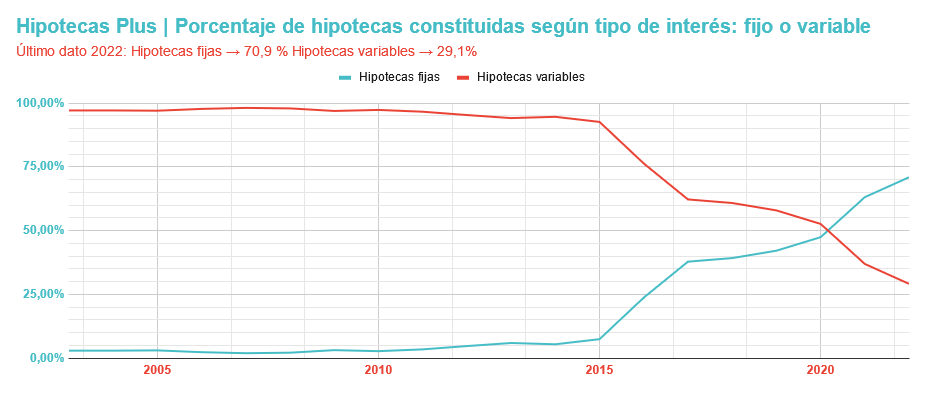

The rise of the Euribor does not affect all citizens with mortgages equally across different European countries. People and families with mortgages in Portugal, Spain, Ireland, and Italy are suffering more from the interest rate hikes ordered by the ECB, as these are European countries where traditionally, mortgages have been contracted on a variable interest basis for many years. However, in Germany or France, contracting a fixed-rate mortgage has been much more common.

The banking sector argues that in Spain, home loans are offered at lower prices than in many European countries, standing at the Eurozone average with a rate of 3.93%, according to data provided by the ECB in September 2023.

In Spain, we find an average rate for mortgages at 3.85%, quite close to the European average. However, how does this compare with the rest of Europe? Malta leads the list as the cheapest country to finance a house, with an average cost of 1.92%, followed by France, Croatia, and Belgium, with rates of 3.36%, 3.54%, and 3.73% respectively.

At the other end of the spectrum, Latvia tops the list of countries with the highest interest rate at 5.82%. Spain, although it ranks as the fifth lowest, as we can see in the ECB’s website chart, follows the upward trend of the European central bank’s official rates and the Euribor. The growth of the mortgage index, currently at 4.160%, impacts mortgages, making them more expensive by an average of about 125 euros per month.

Different Pace from Banks for Mortgages and Deposits

As we can see in the previous chart, banks in European countries have quickly passed on the significant increase in ECB interest rates to mortgages. However, it’s also important to note that this transfer has not occurred as quickly in the payment of deposits.

Spain has suffered more from the impact of the interest rate hike, as it is not one of the countries with the highest income among its citizens.

Despite the perception of lower rates in Spain, the economic reality, with average incomes lower than in the Eurozone, means that we allocate a significant percentage of our salaries to mortgage payments.

Therefore, even though Spain is not the European country with the highest interest rates on its mortgages, having lower average incomes among the population compared to other European countries, it suffers more significantly from the substantial interest rate hikes executed by the ECB.

The rise in interest rates affects both the marketing of variable-rate mortgages and fixed-rate mortgages.

We do not want to conclude this article without mentioning that the interest rate hikes affect both fixed and variable-rate mortgages marketed in all European countries.

A citizen with a fixed-rate mortgage does not experience the interest rate increase when paying their monthly mortgage installment, as it remains constant throughout the life of the loan.

However, if we refer to the marketing of mortgages by financial institutions, the interest rate hike does affect both variable and fixed-rate mortgages: the variable ones are evidently impacted due to the rise in the Euribor, and the fixed ones because banks have to lend money at a higher interest rate than that established for the price of money by the ECB, to avoid lending at a loss.