The Euribor slightly increases in March 2024 to 3.718%

1 April, 2024 | Antonio Beltrán

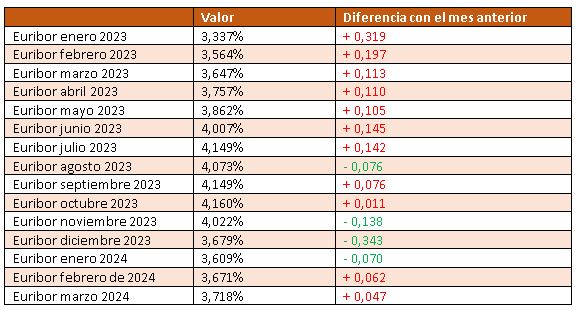

The Euribor increased in March 2024 to 3.718%. This is a slight rise compared to February, which was 3.671%. A year ago, in March 2023, the Euribor was slightly lower than it is now, specifically at 3.647%.

This means that mortgages with an annual review based on March data will become more expensive, but not significantly so since the difference between the current Euribor and that of a year ago is less than half a tenth.

Mortgages reviewed semi-annually WILL become cheaper, since 6 months ago, in September 2023, the Euribor was above 4%, specifically at 4.149%. Now that the Euribor stands at a lower value than it did 6 months ago, mortgages with a semi-annual review based on the March value will have a more affordable monthly payment.

The Euribor is likely to remain virtually frozen for a few months, until there are signs of interest rate cuts by the European Central Bank (ECB).

Interest rates are kept at 4.5% by the ECB

The European monetary institution always acts with caution, although this caution can lead to delayed decisions. It took quite some time to lower interest rates when the economic crisis due to subprime mortgages burst at the end of 2007, although it eventually did so. It began in October 2008, a year after the start of the crisis, and gradually reduced the rates to 0%.

It now seems that it will also take some time to lower interest rates again, even though the economy is already cooling down in Europe and inflation has significantly decreased. In fact, Lagarde predicts that the CPI in the Eurozone will be at 2.3% this year and 2% in 2025.

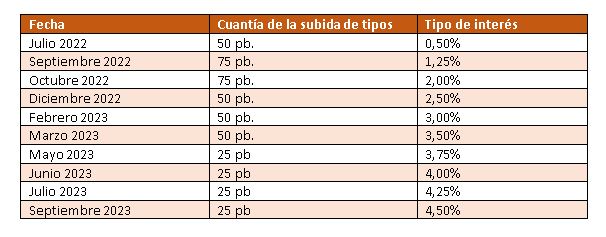

At the latest ECB monetary policy meeting, which took place on March 7, 2024, it was decided again to keep interest rates at 4.5%. Therefore, we cannot add any more lines to the table we presented to you of the 10 increases ordered by the ECB during 2022 and 2023, which led to the spectacular rise in the Euribor.

The ECB wants prices not to increase by more than 2%

The caution with which the ECB acts is explained by its main economic mission: to keep the rise in prices (inflation) close to, but below 2%.

Its fight against inflation is always strict. And it will always do so, even if it means cooling down or slowing the European economy.

The institution decisively ordered interest rates to be raised during 2022 and 2023 in response to inflation in Europe exceeding two digits, as a result of the war in Ukraine and the Covid-19 pandemic.

The ECB now keeps interest rates at 4.5%, due to current inflationary pressures, which, according to ECB statements, are due to a strong increase in wages.

Interest rates will eventually go down

Although the ECB is very cautious, it will ultimately decide to lower interest rates, and the interbank market, which is mediated by the Euribor, is aware of this.