What type of mortgage do Spanish mortgage holders prefer?

5 December, 2023 | M Aparicio

Last Updated on 3 years ago by Antonio Beltrán

From Hipotecas Plus, we suggest reading this article, which discusses what type of mortgage Spanish mortgage holders prefer.

Knowing and understanding the preferences in the Spanish mortgage landscape is very interesting, especially for those looking to acquire a home. It also helps us understand the economic and financial dynamics of our country.

Many consumers considering signing a mortgage undoubtedly face the uncertainty associated with making crucial decisions and need a lot of information, such as knowing what type of mortgage most people choose. It’s about a mortgage, which usually means talking about a lot of money, and it’s not a matter to make light decisions in these cases.

Many future mortgage holders are not only concerned about finding the best conditions for their loan but also about making the right choice when selecting the type of mortgage, that is, choosing between a fixed, variable, or mixed mortgage.

Without further ado, let’s answer the question: What is the most popular choice currently among Spaniards regarding the type of mortgage?

Mixed mortgages!

Evolution of the Type of Mortgage Chosen by Spaniards

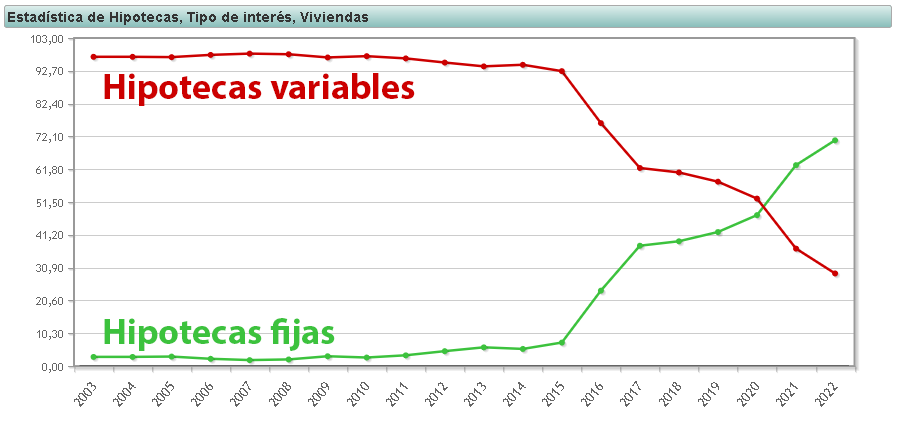

Until 2015, almost all the mortgages marketed in Spain were of the variable type. However, starting from that year, fixed-rate mortgages experienced an upward trend, leading them to surpass variable-rate mortgages in percentage from 2020, and they continued to grow after that year.

The reasons why fixed-rate mortgages have overtaken variable ones are mainly two:

- During the long years of the negative Euribor for banks, financial institutions tried to make fixed mortgages more attractive to ensure a higher profit than with variable ones. With the latter, the entities practically only managed to recover the loaned money and a nearly null interest.

- The economic imbalances caused by the pandemic and the war in Ukraine have led to high inflation, prompting the European Central Bank (ECB) to raise interest rates from 0% to 4.5%. The Euribor, which always follows the trajectory of the price of money, has also risen sharply, driving citizens away from variable mortgages and bringing them even closer to fixed mortgages.

But the problem of high interest rates and consequently a high Euribor affects not only variable mortgages but also new fixed mortgages, which lose the attractiveness they had when the Euribor was below 0.

Banks cannot offer fixed mortgages much below the price of money, because if they do so, they say they are lending their money “at a loss”. Therefore, if variable mortgages become more expensive, inevitably, more expensive fixed mortgages are also offered.

The Success of Mixed Mortgages

For a long time, mixed mortgages were practically residual, but now, we can consider them the queens of mortgages. They are the most chosen among Spaniards. Why are mixed mortgages now so successful?

Previously, mixed mortgages seemed to only make sense in helping the banks, as they were sold with a fixed rate at the beginning of the mortgage for one or a few years, and then it switched to variable. It gave the impression that the bank wanted to offer a fixed rate initially to escape from a Euribor buried in the negative zone, to then switch to a variable mortgage with a higher Euribor after some time.

However, now mixed mortgages have gained a lot of attractiveness because, in general, they offer a fixed rate with a lower interest than some fixed interest rate mortgages, for much longer than before, 10 years, and then it turns into a variable with a differential over the Euribor that in many mortgages turns out to be attractive.

Thus, mixed mortgages have surpassed the options of some fixed and variable ones and represent 68.88% of the mortgages signed in September 2023. The trend has been increasing since November 2022 and has even dethroned the previously favorite, the fixed mortgage.

According to a study by a comparator in the third quarter of 2023, the mixed mortgage consolidates as the preferred choice for mortgage holders in Spain, accounting for almost 70% of the total signings each month.

Other Interesting Data About the Current Mortgage Market

The same study mentioned above indicates that the profile of today’s digital mortgage holder is, on average, 37.48 years old, with an average job tenure of 7 years, a permanent job, and a net monthly income of 2,746 euros. Typically, the mortgage is purchased as a couple, and they have average savings of 92,827 euros.

From Hipotecas Plus, we want to point out that not having these conditions doesn’t mean the bank will refuse to approve your mortgage, but it is very important to have good financial health and especially to have savings. The more economic stability you have, the better conditions you will find to negotiate with the bank and obtain advantageous terms for yourself.

Updated Mortgage Data

To understand the success of mixed mortgages, let’s look at data from mortgages that are currently being marketed and advertised.

We have chosen the fixed, variable, and mixed mortgages from Openbank and EVO. All the following mortgages have a capital of 100,000 €, a term of 25 years, and are NON-bonified mortgages.

Openbank Mortgages

- Open Fixed Mortgage: APR ? 3.82%, installment of €581

- Open Mixed Mortgage: APR ? 4.14%, APR for the first 10 years 3.24%, then Euribor +1.05%

- Open Variable Mortgage: APR ? 5.28%, installment of €593

Evo Mortgages

- Intelligent Fixed Rate Mortgage: APR ? 4.04%, installment of €593

- Intelligent Flexible Mortgage: APR ? 3.89%, APR for the first 15 years 3.35%, then Euribor +1.15%

- Intelligent Variable Mortgage: APR ? 4.91%, installment of €577

The most logical explanation we find for the current attraction of mixed mortgages is that they allow the consumer to escape the current high value of the Euribor for a long period, 10 or 15 years, at a better interest rate than a fixed mortgage.

After that time, the mortgage will switch from fixed to variable, but perhaps many of those with mortgages have taken out a mixed mortgage, thinking that by then they may have been able to cancel their mortgage, for example, by making partial repayments during the fixed period.

Other articles from Hipotecas Plus that might interest you

Fixed, Mixed, and Variable Rate Mortgages, an article by the Bank of Spain